How to Choose the Right Pet Insurance Plan in Kenya

Introduction

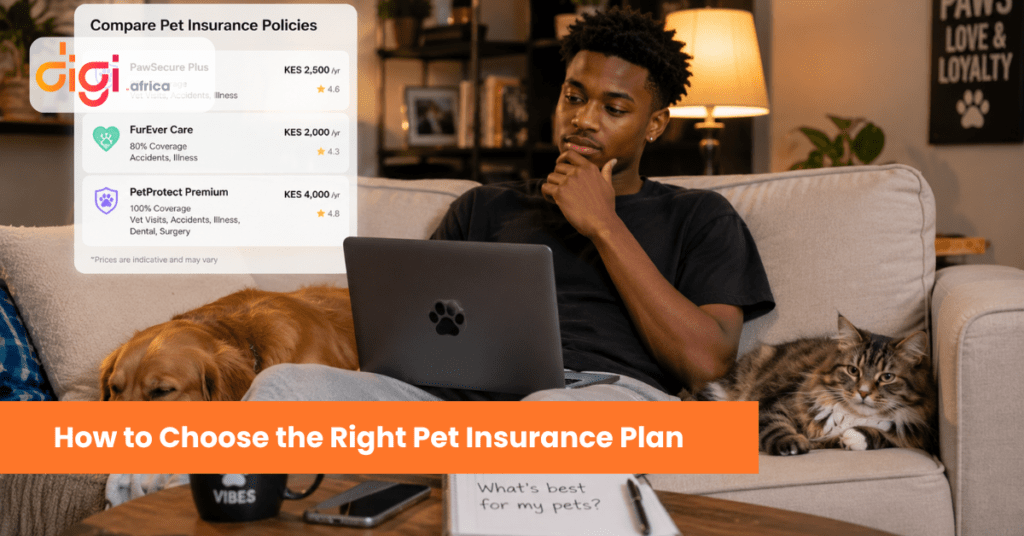

Choosing a pet insurance policy can quickly feel overwhelming. When you begin comparing options in the market, you will notice that while almost every brochure features a picture of a smiling puppy or a healthy cat, the fine print underneath those images varies drastically.

Some policies are designed strictly as a financial shield against sudden, catastrophic accidents. Others function as comprehensive medical covers that step in for infections, chronic illnesses, diagnostics, and complex surgeries. Selecting the wrong option doesn’t just put your savings at risk during a crisis, it can mean your fur-baby misses out on life-saving veterinary care when every second counts.

Finding an affordable pet insurance plan in Kenya that actually delivers when you need it requires an objective approach. This guide cuts through the corporate jargon to show you exactly how to choose pet insurance that aligns perfectly with your pet’s specific biological needs, your lifestyle, and your household budget.

Why Pet Insurance Matters

The veterinary landscape in Kenya has advanced significantly. Local clinics now boast top-tier diagnostic equipment, overnight intensive care units (ICUs), and highly specialized surgical teams. While this allows us to treat conditions that were untreatable a few years ago, the price of modern veterinary medicine has mirrored human healthcare inflation.

A single medical emergency, such as a dog swallowing a toy or a cat contracting an acute bacterial infection, can quickly result in a vet bill ranging from KES 30,000 to over KES 100,000.

Securing the best pet insurance plan transforms these highly stressful, unpredictable financial shocks into a structured, predictable monthly premium. Ultimately, a proper policy ensures that you can focus entirely on your pet’s recovery, rather than staring at a hospital invoice wondering how you will pay for it.

Understand the Different Types of Pet Insurance

Before you can compare pet insurance plans, you must understand the three core structural categories available in the market today.

1. Accident-Only Cover

This is the most baseline, budget-friendly tier of pet insurance. It is built strictly to handle sudden, physical trauma caused by external factors.

- What it covers: Bone fractures, snake bites, road accidents, poisoning, and deep lacerations from animal fights.

- What it ignores: Any form of illness, such as tick fever (biliary), respiratory infections, or stomach bugs.

- Best for: Budget-conscious pet parents who have a healthy, young animal and simply want a baseline safety net against unexpected external mishaps.

2. Accident & Illness Cover

This is the modern standard for the majority of urban pet parents in Kenya. It strikes a balance between cost and robust, practical utility.

- What it covers: Everything in the accident tier, plus acute and chronic illnesses, viral infections, emergency surgeries, tumors, and internal metabolic issues.

- Best for: The vast majority of dog and cat owners who want a reliable shield against both freak accidents and sudden medical diagnoses.

3. Comprehensive Pet Cover

This is the premium tier of pet medical insurance in Kenya. It aims to bundle emergency care with ongoing lifestyle and wellness management.

- What it covers: Accidents, complex illnesses, and potential add-ons for routine wellness, such as specific dental treatments or congenital breed extensions.

- Best for: Owners of high-value pedigree breeds or pet parents who want the absolute maximum layer of financial protection available.

What Does a Good Pet Insurance Plan Cover?

When reading through a policy document from underwriters like APA Insurance or GA Insurance, use this checklist to verify that the pet insurance coverage explained gives you actual protection:

- Accidents and Injuries: Immediate coverage for trauma, including emergency vet consultation fees.

- Illnesses and Diseases: Coverage for common local ailments like tick fever, parvovirus, and respiratory issues.

- Surgery and Anesthesia: Full payment support for theater fees, surgeon costs, and post-operative medications.

- Diagnostic Tests: Crucial coverage for costly modern diagnostics like digital X-rays, full blood panels, and scans.

- Hospitalization: Coverage for the daily room rate if your pet needs to be monitored overnight on an IV drip.

- Straying and Theft: Financial compensation if a pedigree pet is stolen or goes missing and cannot be located after a set period.

Check the Pet Insurance Policy Exclusions Carefully

The true value of an insurance policy is found in what it excludes. To build a relationship of trust with your provider, you must review the fine print for these common industry exclusions:

- Pre-Existing Conditions: No insurance company in Kenya will cover an illness or injury that your pet showed signs of before the policy was signed. If your dog is already being treated for a skin allergy, any future treatment for that specific allergy will be paid entirely out of pocket.

- Lack of Vaccinations: If your pet contracts a preventable disease (like Parvovirus or Feline Leukemia) and your vaccination certificates are not up to date, the insurer will deny the claim.

- Cosmetic or Elective Procedures: Tail docking, ear cropping, or cosmetic dental cleanings are completely excluded.

- Breeding and Pregnancy: Costs associated with whelping, emergency C-sections, or puppy care are typically excluded unless you purchase a dedicated commercial breeder’s rider.

Understand Pet Insurance Coverage Limits & Co-Payments

When you look past the premium price, you need to understand three core financial metrics that dictate your actual out-of-pocket costs during a claim.

Annual Policy Limits

This is the maximum amount the insurer will pay out over a 12-month period. For example, if your plan has an annual veterinary expense limit of KES 75,000, any medical costs incurred beyond that KES 75,000 within that year must be covered by you.

Deductibles and “Excess”

In Kenya, most pet policies operate with a standard “excess” clause, usually around 10% of each and every claim (or a minimum flat fee like KES 2,500). If your vet bill comes out to KES 30,000, a 10% excess means you pay KES 3,000 at the clinic, and the insurer covers the remaining KES 27,000.

Key Takeaway: Plans with incredibly cheap premiums often hide a much higher excess percentage (e.g., 20%) or lower annual limits. Never buy based on the monthly premium alone.

Consider Your Pet’s Breed, Age & Lifestyle

Your pet’s specific profile should directly dictate how you choose the right pet insurance plan.

- The Age Factor: The ideal time to buy pet insurance in Kenya is when your animal is a young puppy or kitten (starting around 12 weeks to 6 months old). Their premiums will be at their lowest, and their medical history will be completely clean, preventing any pre-existing condition exclusions.

- The Breed Risk Profile: Purebred dogs like German Shepherds are biologically prone to hip dysplasia, while Bulldogs often face respiratory issues. If you own a pedigree animal, look for a comprehensive policy that offers higher maximum medical limits to offset these known genetic risks.

- The Lifestyle Risk: If you have an active, highly adventurous outdoor dog who frequents social dog parks, their risk of accidents, bite wounds, and parasite exposure is higher than a strictly indoor cat, making an Accident & Illness plan essential.

Compare Waiting Periods

A common mistake pet parents make is buying a policy on a Friday and trying to claim for a sick pet on a Monday.

Pet insurance plans utilize waiting periods, a specific window of time at the start of a policy during which you cannot make a claim. This prevents individuals from fraud, such as buying insurance only after their pet falls ill.

- Accident Waiting Periods: Usually short, typically activating within 24 to 48 hours of policy inception.

- Illness Waiting Periods: Generally range between 14 and 30 days. Any illness that manifests during this window will not be covered.

Questions to Ask Before You Buy Pet Insurance

Before signing a proposal form, call your broker or insurance representative and run through this direct checklist:

-

- Is a formal veterinary health and valuation report required before the policy goes live? (Most local underwriters require a certified vet check and a microchip for identification).

- What is the exact excess percentage or flat fee structure for a medical claim?

- Are emergency midnight consultations covered under the veterinary expenses limit?

- Does this policy include third-party liability if my pet causes damage or injury outside our home?

- What is the average turnaround time for claim reimbursement? (A good standard in the local market is roughly 7 working days once all documentation is submitted).

Common Mistakes Pet Owners Make

- Playing the Waiting Game: Waiting until your pet shows signs of slowing down or gets into their first minor scrape. By then, their medical records will lock out key coverage as pre-existing.

- Ignoring the Vet Network: Assuming every clinic accepts direct payment. Always check if you need to pay upfront and claim reimbursement, or if your provider has direct settlement links with major local veterinary hospitals.

- Choosing Solely on Price: Opting for an ultra-cheap plan only to find out during a crisis that it doesn’t cover diagnostic X-rays or prescription medication.

Final Thoughts

There is no singular “one-size-fits-all” answer when deciding which pet insurance is the best. The right plan is the one that fits neatly into your monthly budget while providing enough medical head-room to cover a major veterinary crisis without financial strain.

By analyzing the exclusions, matching the coverage to your pet’s age and breed, and understanding the fine print regarding policy excess, you can secure true peace of mind. Taking the time to choose wisely today ensures that you can always provide the highest standard of care for your companion when it matters most.

Frequently Asked Questions

1. What should I look for in pet insurance?

Prioritize checking the illness exclusions, the annual maximum limit, the waiting periods for illnesses, and the exact “excess” percentage you will be required to pay out of pocket per claim.

2. Is pet insurance worth it in Kenya?

Yes. Given that a single diagnostic run and emergency surgery can easily surpass KES 50,000, a predictable annual or monthly premium protects your household from sudden, catastrophic financial stress.

3. What does pet insurance usually cover?

Standard plans cover veterinary costs arising from unexpected accidents, injuries, sudden illnesses, emergency surgeries, diagnostic lab work, and third-party civil liability.

4. Does pet insurance cover vaccinations?

No. Routine preventative care such as annual boosters, deworming, grooming, and microchipping are considered standard pet maintenance and are paid for out of pocket.

5. When is the best time to insure a pet?

The absolute best time is when your pet is a healthy puppy or kitten (from 12 weeks of age onwards). Insuring them early locks in lower premiums and avoids pre-existing condition exclusions.

Protect Your Pet With the Right Cover

Give your companion the protection they deserve and safeguard your budget from unexpected veterinary expenses. Explore pet insurance options tailored specifically to your lifestyle and your pet’s needs.

Get a Custom Pet Insurance Quote Today